competition

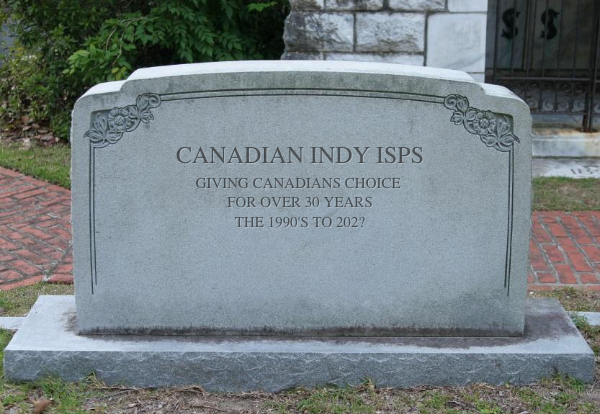

Canadian Independent ISPs - another one bites the dust

One topic I've been meaning to write about for some time now is the increasing number of independent ISPs who have been acquired by incumbents.

As we start 2023, I was saddened to learn today that another Canadian independent ISP, start.ca has been acquired by Telus. While the transaction wasn't announced publicly, it was confirmed by Telus after inquiries from MobileSyrup. This is standard practice for Telus who often keep their ownership of some of smaller providers hidden, like they did with Radiant until putting it under the GoCo banner. Start.ca was an amazing story - started in 1995 in London, ON they grew to become a large nation-wide wholesale provider. And over the past few years they have been deploying their own fibre optic network in the London area, bringing true high-speed internet to residential and business customers at very affordable rates. A true Canadian telecom success story.

Last year (2022) was ripe with these incumbent acquisitions - Bell acquired EBOX, a Quebec based ISP, and Distributel (who also owns my "alma mater" Primus Canada) for an undisclosed sums. Quebecor also acquired VMedia in 2022 as part of its plans to expand its presence across the country. Telus also did some shopping and picked up Altima in June 2022 as well as RhiCom Networks, a fibre provider in the Kamloops area. And I'm sure I missed some of the smaller acquisitions that happened - often these companies are acquired without any public announcements as the valuation is too low to involve any regulator.

Not all the independent ISPs are gone yet - there are a few big names left, notably TekSavvy and Oxio but they are also facing an uphill battle to survive. As I pointed out in a recent post, the "flanker brand" ISPs are atacking them head on using predatory pricing. Combine this with the continued regulatory uncertainty around access to fibre to the home networks and its hard to see a path for them to continue to grow. The writing however appears to be on the wall - without strong intervention by the CRTC I just can't see a path for these companies to continue to exist in a few years.

So what does this all mean for Canadian consumers? For the next few years its likely that Bell and Telus will continue to operate these former independent ISPs as separate business units but offer them access to sell products like fibre to the home that are currently out of reach of other ISPs. Consumers will continue to benefit from some lower prices, which is a small win, but over time, as the last of the remaining ISPs die off, I envision them turning into just another flanker brand of an incumbent, like Virgin or Koodo and pricing increasing as the threat of wholesale competition is removed.

On the regulatory front this also has major implications as the number of parties willing to engage the CRTC to advocate on behalf of independent ISPs is now smaller than ever. With no one to help fund the fight how will any small ISP survive? Organizations like the Internet Society, Canada Chapter (of which I'm the vice-chair) will continue to exist and attempt to fight, but we're just a bunch of volunteers. We don't have the time, resources, or budget to fight at the level that is required.

For me, this is all just flat out depressing. Having started at my first dial-up ISP in 1994 doing technical support I've seen the innovation and ingenuity smaller ISPs provide first hand for almost 30 years. In 2019 the industry had hope - the CRTCs rate decision lowered wholesale rates by as much as 72 percent. We finally had rates that made it possible to offer residential internet service at a decent margin. But that hope was quickly lost as appeal after appeal by the incumbents stalled the implementation of the rate reductions until the CRTC basically reversed them in 2021. From that moment on the script had already been written - with the 2021 rates and no real access to fibre to the home networks, these independent ISPs really only had one choice - get acquired or die trying.

Topics: